The New York Pied-à-Terre Tax: What Condo & Co-op Sellers Need to Know

Published June 8, 2026 by Fox Rothschild LLP

What Is It?

New York State has enacted a new annual tax — officially called the "City Surcharge on Property That Does Not Serve as a Primary Residence," commonly known as the Pied-à-Terre Tax (PAT) — effective July 1, 2026. It's an add-on to existing property taxes, not a replacement. foxrothschild .

Who Does It Hit?

It applies to condo,co-op, and Townhouse owners who:

Don't use the unit as their primary residence, AND Own a unit valued above $1 million.

In plain terms: A buyer is affected if they're purchasing a pied-à-terre, investment unit, second home, or foreign-owned apartment. Sellers will be affected, as the resale value of homes in 2026 will deter pied-a-terre buyers at certain price points by increasing the annual carrying costs of these homes.

The following appear to be exempt from Pied a Terre Designation, therefore triggering a tax:

The apartment is owned by a natural person and occupied by that person or an immediate family member (spouse, child, sibling, parent, grandparent or grandchild) as their primary residence. Primary residents (or immediate family members living there)

The apartment is leased for at least one year to an arm’s length lessee (a natural person) who maintains the apartment as their primary residence (the lease and occupancy must be in effect as of January 5th of the immediately preceding fiscal tax year). Landlords who lease the unit for at least a year to a primary-residence tenant.

The apartment is owned in a trust and the beneficial owner of the trust occupies the apartment as their primary residence but only if the beneficial owner is the sole beneficiary.

The property is owned by a partnership, corporation or LLC and the apartment is the primary residence of the majority owner, or in certain other circumstances. Trust or LLC owners where the unit is genuinely a primary residence for the majority owner

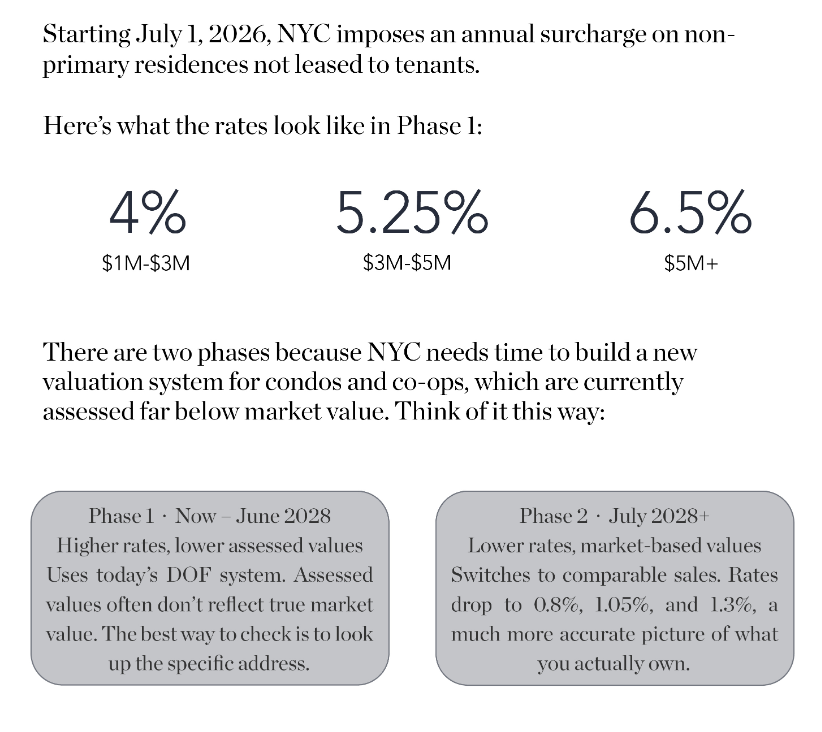

How Much Is the Tax?

In 2026 the tax will be imposed based on Phase 1 calculations. Phase 1 (tax years 2026/27 and 2027/28), based on Department of Finance (DOF) assessments translated to market value:

$1M–$3M valued unit: 4% annually

$3M–$5M valued unit: 5.25% annually

Over $5M valued unit: 6.50% annually

Phase 2 (starting 2028/29), based on comparable sales, or free market closed sale prices:

$5M–$15M: 0.80%

$15M–$25M: 1.05%

Over $25M: 1.30%foxrothschild

Note that Phase 1 rates are strikingly higher — this is because Phase 1 uses city assessment methodology, which tends to undervalue properties relative to actual market prices. To learn what your properties’ assessed value is, and how that corresponds with property taxes, please reach out.

What Does This Mean for Sellers?

For condo sellers: Your buyer pool of non-primary-resident purchasers (pied-à-terre buyers, investors, international buyers) is now facing a significant new annual carrying cost. This could affect demand, negotiating leverage, and your pricing strategy.

For co-op sellers: The risk is more complex. In a co-op, the PAT is charged to the entire building (which has only one tax lot). If a shareholder doesn't pay, the DOF can place a lien on the entire building — meaning the co-op could effectively become a guarantor for a noncompliant shareholder. Co-op boards are already scrutinizing non-primary-residence purchasers more carefully, and this tax gives them additional reason to do so. foxrothschild Cooperatives face unique risks: If a co-op shareholder doesn’t pay the tax, the NYC Department of Finance can place a lien on the entire building — potentially making the cooperative a guarantor for noncompliant shareholders.

What's Still Unknown?

The NYC Department of Finance has not yet issued regulations, so many details about implementation remain unclear — including how estates, trusts with multiple beneficiaries, and layered LLC ownership structures will be treated. The law was passed quickly as part of the state budget, and the practical guidance is still catching up. foxrothschild

The Bottom Line for Your Listing

This tax is real, and it’s implications will be visible in the 2026 market and beyond. If your unit would appeal to non-primary-resident buyers, this tax is now part of their carrying cost calculation and should be part of your pricing conversation. Buyers will factor it in — so it's better to get ahead of it than to be surprised at the negotiating table.

This summary is for informational purposes only and does not constitute legal or tax advice. For guidance specific to your situation, consult a licensed attorney or tax professional.